How Does Personal Credit Affect Business Credit And Financing?

Can You Still Qualify For Business Financing With Bad Credit?

As we speak with hundreds of business owners a week this is one thing that we always get asked on a routine basis…

“Can I still qualify for a business loan even though I have some credit issues?”

The short answer is “yes.”

There are two things I want to discuss first.

One, there are significant differences between a business line of credit and getting a business loan.

A) Interest rates- With a business loan the interest rate is usually fixed, or it’s a fee based loan. With a business line of credit, the interest rate is most likely variable as they are typically tied to the prime rate.

B) Payment Scheduled – Business loans have monthly, weekly, or daily paybacks scheduled with a set number of payments. Sometimes term loans offer quarterly payments as well. For a business line of credit, the amount of the minimum required payment may vary monthly, based on the amount that has been drawn in the previous 30 days.

C) Term- A business loan has a variety of terms based on the type. I’ve seen anywhere from 3 months to 10 years. For a line of credit, the term may be something like 10 years with a option for extension or the bank to call the line due on an annual basis. You’ll want to be careful with this.

D) Fees- Typically bank loans involve fees such as a processing fee, credit fee, and appraisal fee if you take the traditional method of lending. For a line of credit there are typically no fees or there may be a small fee each time the business owner draws from the line.

Read More: If You Need Credit Help Click Here To Get A Free Credit Blueprint

Two, it’s important to point out that credit scores are an important factor to a bank when deciding whether to offer a small business loan or any small business financing.

Each lender has their specific requirements, but according to the U.S. Small Business Administration credit scores reflect how well you handle money. In turn, they will use this to interpret a low credit score as an applicant not possessing the proper skills to manage their finances. If you have poor credit, however, you can still qualify for small business financing, but there only a few products that will fit within those guidelines.

Personal credit scores work for business loans the same way as with any other type of lending. Realistically, anything less than a 660 translates to you having a hard time finding an “A” bank lender with favorable terms. A score of 720 or higher, however, gives you a much better shot at an approval with favorable rates and terms.

This means going to the WellsFargo, Bank of America, or Chase down the street with a 620 FICO will prove to disappoint you as a business owner. Many times they’ll put you through the due diligence which takes up to 3 months, only to come back to you with a declination, after you’ve provided everything in your life except a blood sample.

Going the traditional banking method ends in a bunch of heartache and disappointment. However, there are many different alternative lending methods we can discuss.

But I want to dive a bit deeper into what type of financing you can qualify for with good credit and with bad credit.

Let’s start with SBA loans.

1) SBA Loans

Everyone wants to qualify for an SBA loan because of the great terms and rates. Fundamentally, SBA loans are a small niche product that few business owners qualify for.

The reason so many business owners fail at obtaining an SBA loan is due to the fact that nearly everything in your business and your personal life (financially speaking) must be perfect.

Here’s a quick snippet of SBA guidelines to even be considered for approval:

A) SBA Loan Application – Form 1919

B) Personal Background and Financial Statement SBA Form 912 and 413

C) Profit and Loss Statement

D) Proforma

E) Ownership and Affiliations

F) Business Certificate/License

G) Loan Application History Detailed

H) 3 Years Business Income Tax Returns

I) 2 Years Personal Income Tax Returns

J) Resumes For Each Principal

K) Business Overview and History

L) Business Lease

M) Personal and Business Credit Report

Here’s what they don’t tell you though…

Everything must be perfect.

You’re not typically going to be approved or even considered if you don’t have over a 700 FICO score and that’s if all your financials line up.

In 2013 the average SBA loan was $330,000 and only 13% of applicants were approved.

Those are pretty pathetic numbers.

So for SBA loans, you will not be approved if you have bad credit. But honestly, the amount of headaches and time it takes to actually fund the deal sometimes outweigh the rate and terms they provide small business owners.

2) Alternative or Revenue Based Loans

There are many alternative ways to get business loans.

There’s everything from revenue based loans, to stock based lines of credit, asset based loans, and even merchant cash advances. O

ne of the best products out of those is business revenue lending.

Business revenue lending is a fairly new financial product for business owners.

This type of financing came about when there was a big credit crunch in the U.S. and business owners literally could not access any capital for business growth.

This type of financing really relies on one fundamental thing the business is doing…

Depositing money into the business bank account.

A business revenue lender will look at the past 6 months or so of a business bank account and determine if the business is an attractive lending risk based on the consistency of deposits. Both the volume in number of deposits and dollars deposited. You’ll typically want to have more than 5 deposits a month with greater than $10,000 in monthly revenue generated in the business.

The above will give the business owner the best opportunity for approval.

Here’s how credit affects business revenue loans

A business owner can qualify for business revenue loans regardless of personal credit.

Many entrepreneurs can qualify for this type of loan even if they have 500 credit.

But… you must have steady cash flows.

The business owner who has 700 credit will qualify for much more favorable terms, and the amount of approval will be higher than the business owner with 500 credit.

Credit scores and terms/conditions/rate have a correlated relationship.

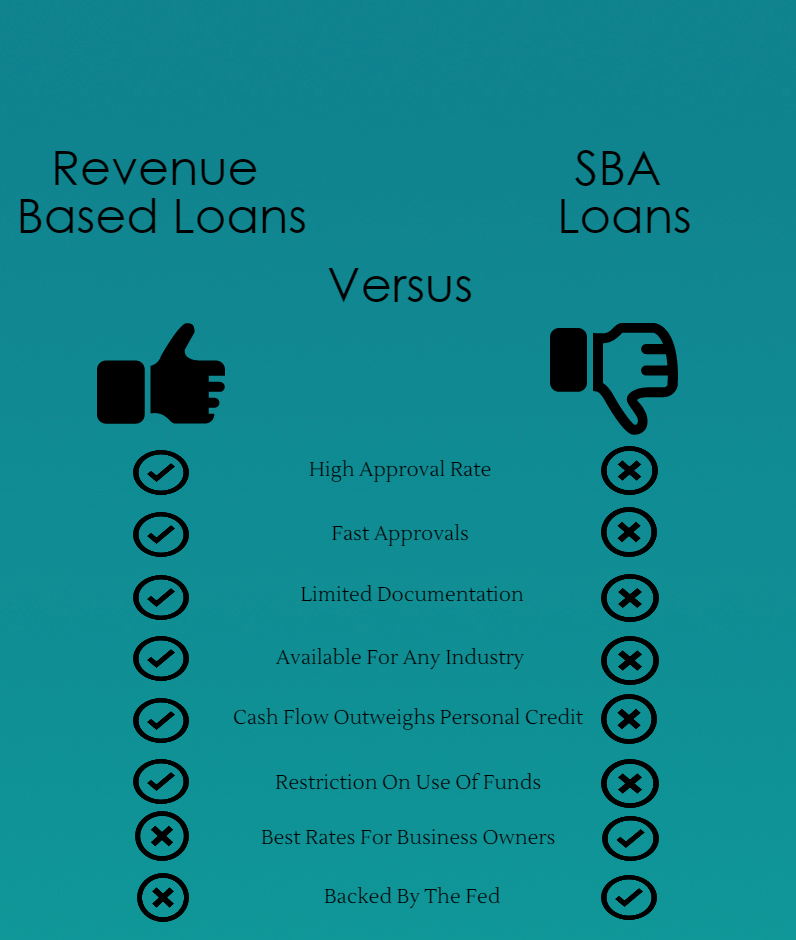

Here’s a comparison of revenue based loans versus SBA loans:

The pros typically outweigh the cons when it comes to business revenue loans.

How does personal credit affect business credit and financing?

For business revenue loans the answer is it only affects the approval amount, not necessarily the approval itself.

Now I want to cover what absolutely cannot be on the credit report for any type of financing:

1) Any bankruptcy that has not seasoned atleast 6 months- Really, you’ll want it seasoned atleast one full year, but if the business is very strong there are a few lenders that will take a look.

2) Unpaid Tax Liens – Lenders typically aren’t in the business of paying off other debt or consolidating it. If structured payments are in place or you’ve spoken with an enrolled agent you’ll want to be sure to get that on paper before attempting to qualify for a small business loan.

3) A felony- On a rare occasion, a convicted felon can qualify for a small business loan. However, anyone who has ever been convicted of bank fraud, wire fraud, money laundering, embezzlement, racketeering or any crime related to finance, the probability of an approval is virtually zero.

There’s little tolerance for financial fraud for any lender, regardless of when it occurred.

One of the benefits of alternative methods of lending is not diving into debt ratios, tax returns, profit and loss statements, and balance sheets.

Alternative lenders look at cash flow.

As an alternative lender, Bentley Capital Ventures knows that “books” don’t always show exactly what’s going on.

Business owners write off everything, so we disregard tax returns.

Other lenders only ask for tax returns.

So each lender has their own niche.

For this reason, it’s important to have a written business plan in place.

A written business plan, written correctly, can overcome things like credit when it comes to venture capital financing, or private money.

We see it happen all the time.

Conclusion

When it comes to personal credit and how it affects a business owners ability to access credit and financing, it really comes down to a few factors.

If you go the traditional route, credit will 100% have a role in your approval.

The non traditional route, using an alternative lender, does allow some room for credit hurdles depending on the type of financing you’re approved for.

You’ll want to be sure to find out everything you can about all the options available before determining if your credit needs to be 100% perfect before moving forward.

Questions? Call Joe Schuck: VP of Sales

813.734.7176